Date: 19 July, 2019 - Blog

Over S1, the CAD has bested all its G-10 peers and by a quite a distance thanks to the oil price recovery from their 2018 lows and the domestic economic rebound. The CAD outperformance has been a consistent theme over the last month and should continue.

Some months ago, many G-10 central banks were ready to raise rates this year. However, things have strongly changed. Central banks in Australia and New Zealand have both already cut rates this year and should do it again. The ECB will move in September. And the most notable, the Fed which will lower its Fed Funds rate by 25 bps this month and again later in the year.

However, the Bank of Canada is not dancing on the same foot

Last week, even if Governor Poloz refused to cheer too loudly about recent Canadian economic improvement, it did not turn dovish. The BoC base case scenario could be described as an all-clear outlook ahead. However, it is becoming somewhat more concerned about risks. The BoC could have taken an even sunnier. Instead, it chose to downplay some of the Q2 temporary upside surprise.

A few months ago, Poloz mentioned that the most likely next move will be a hike rather than a cut. Last week, he talked about rates being appropriate, and that they would respond if headwinds dissipate or worsen. That is a more nuanced statement that leaves room for a move in either direction.

There is no immediate pressure on the BoC to cut rates, even if the Fed will do it. That reflects the fact that Poloz raised rates more cautiously than his US counterpart. Unlike the White House, Canadian officials are not pushing for a rate cut, and markets are not in a hurry to price in such a development this year. Lower bond yields have helped to stabilize the housing market without lowering key rates.

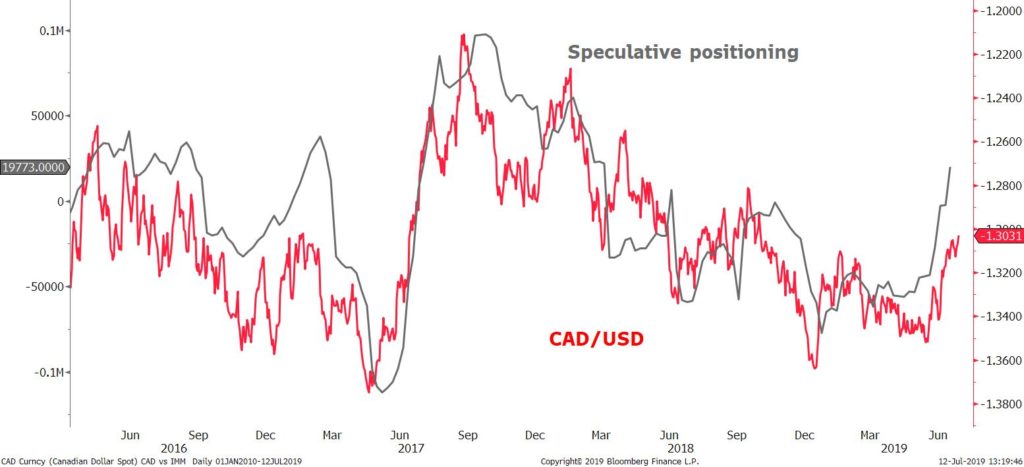

CAD and speculative positioning

- Clearly, the BoC is in no hurry to adjust its key rates in either direction. It asserts that its stance remains appropriate