Date: 11 March, 2021 - Blog

When the best is the enemy of the good

Vaccination is accelerating, paving the way for a gradual reopening of the economy from Q2 and a herd immunity by year-end in lots of countries. Economic recovery will sharply accelerate. The new American administration is re-establishing many international links and is restoring its credibility. Italy avoided a political crisis by appointing a technocrat maestro.

All these developments have resulted in a significant rise – about 50 bps – of long-term bond yields in a short period of time (about a month). Per se, this spells a welcome confirmation that recession and deflation risks belong to the past. This will also relieve some pressure on pension funds and life insurance to match their long-term liabilities. Savers and banks would also applaud. But, ultimately, such a multiplication of good news is creating a snag for policymakers and central banks. Indeed, their capacity to maintain ultra-low rates, for a very (very) long time, is under careful markets’ scrutiny.

The pursuit – if not the essence – of financial repression is challenged

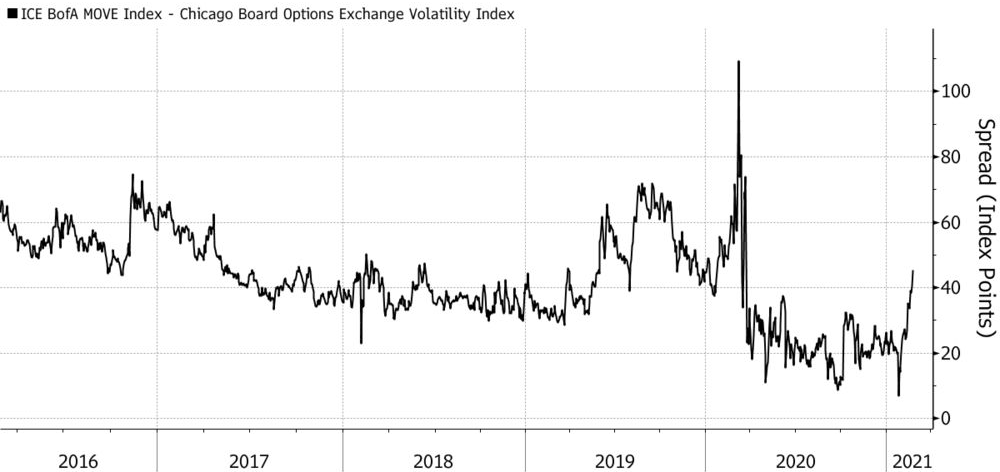

End of bonds’ artificial coma

The cost of ensuring / protecting bond portfolio, i.e. the Move index, collapsed in the aftermath of the pandemic. It even remained below the 20 mark for numerous months last year. But the resurgence of adverse developments in the US bond market, not only at the very long end of the curve, is definitely shaking the fixed income boat. This is clearly visible with the sharp rise of the index above 40 in just a few days.

Source: Bloomberg

This represents a warning signal for central bankers. They cannot any longer just obfuscate and kick the can down the road, when addressing markets. Actually, this is not just a US story. European and Japanese yields also experienced adverse developments. For now, the ¨damage¨ for global and long-term oriented investors, like endowments, pension funds, and global balanced managers has been very limited, if any. Still, for awfully long duration segments the story is different. For example, a few high-flying IT stocks, among them Tesla, corrected by more than 20% from recent highs. Similarly, the iconic Austrian century bond – maturing in 2117 – experienced a fall of similar magnitude.

Source: Bloomberg

- Markets are entering the learning zone

- In doing so, they challenge financial repression

- World policymakers must urgently adapt / recalibrate their policies