Date: 7 August, 2023 - Uncategorized

It’s been a while…

¨Productivity measures the amount of value created for each hour that is worked in a society.¨ Mc Kinsey

Basically, on a long-term perspective, ∂Real Growth = ∂employment + ∂productivity. Unfortunately, both contributors disappointed last decades. The labor markets’ growth suffered from population ageing and the levelling-out in labor force participation. Productivity disappointed for – cyclical – reasons, essentially underinvestment in capital during the financial repression and insufficient public investments in education and innovation skills… See charts 1 & 2. Additional obstacles surfaced last years linked to ground of reinforced sovereignty: a) barriers on trade and on mobility of skilled labor, b) embargos on strategic technologies, re-onshoring, lower FDIs, c) scarcer natural resources on the (energy/rare earth/food).

Economists have been split for years regarding perspectives of productivity. The ¨techno-pessimists¨ argued that the latest wave of digital developments will fail to raise labor productivity because related innovation essentially spells ¨distraction effect¨ (say Netflix/Instagram overuse). The ¨techno-optimists¨ reply that adaptation of infrastructure and processes takes more time with new technologies. Beyond this controversy, the outburst of easily accessible Generative Artificial Intelligence products/solutions sends them back-to-back.

No natalist policy can materially impact on labor markets in the short to medium-term

Therefore, in the years ahead, boosting growth desperately spells raising productivity for policy-makers

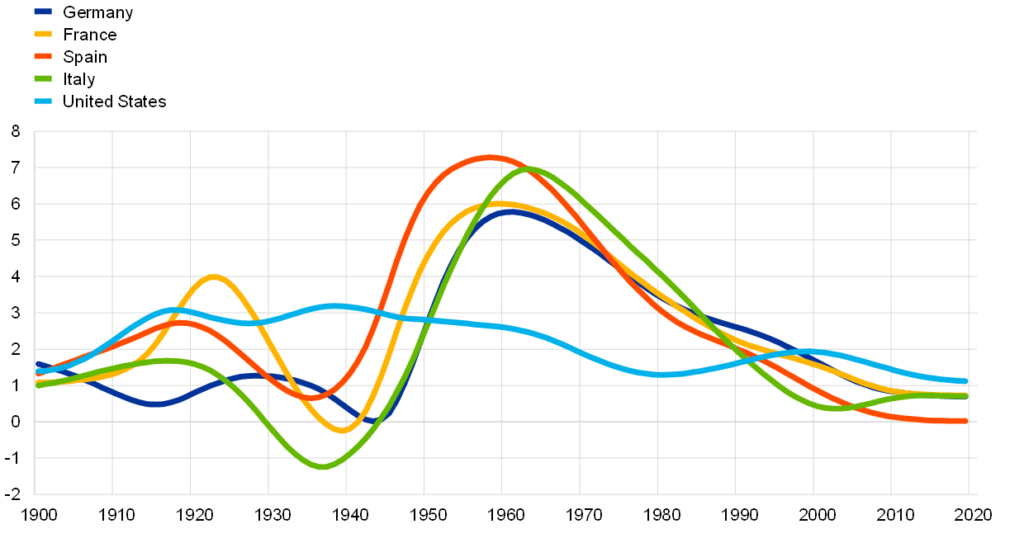

Chart 1: A comprehensive decline in productivity

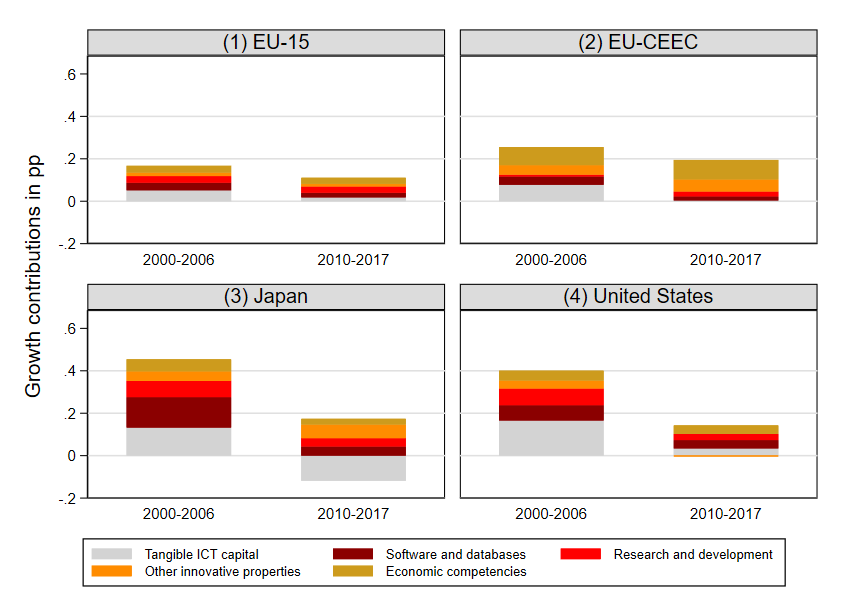

Chart 2: Contribution of capital to productivity

A disappointing first wave of Digital Transformation

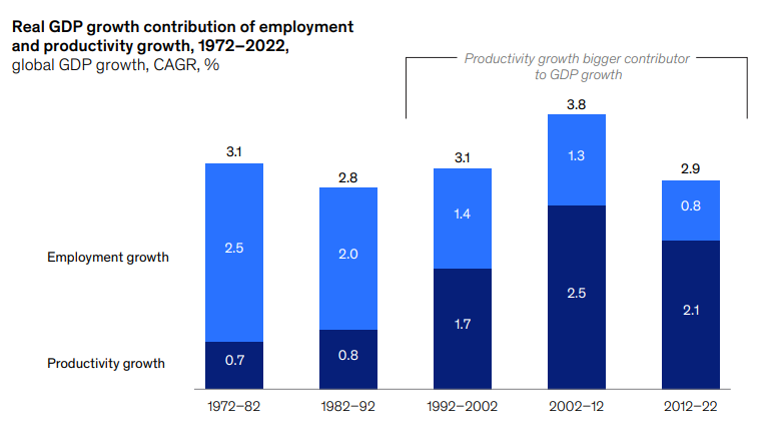

A Digital Transformation (DT) of economies has been underway for several years now, including the first generation of AI. DT has gradually disrupted traditional business models, by surprising and delighting customers with new services in online banking/retailing, streaming, autonomous driving features on cars, etc. Disrupted companies have been revisiting their business models in an open-ended process. DT has also deeply transformed the structure of labor markets, through work at home. Despite more than a decade-long of digital innovative developments, OECD economic growth has remained low. Granted, the essential cause is demography, as the compound growth of worldwide workers slowed from 2.5 to just 0.8 percent between 1972–82 and 2012–22. But elevated hopes for productivity gains have also been totally dashed! Last decade, productivity growth… slowed by 0,4% versus the former decade. See chart 3.

But aren’t we really on the verge of a second hastening underway with the outburst of GAI products / solutions? Hence the multi bn$ question: could GAI be, finally, the long-awaited ultimate game-changer?

So far, buoyant DT has not improved productivity

Chart 3: Weaker structural drivers of growth

How could GAI impact on productivity?

¨ Generative Artificial Intelligence refers to a category of AI algorithms that generate new outputs based on the data they have been trained on. They use a type of deep learning called generative adversarial networks and have a wide range of applications, including creating images, text and audio.¨ WEF

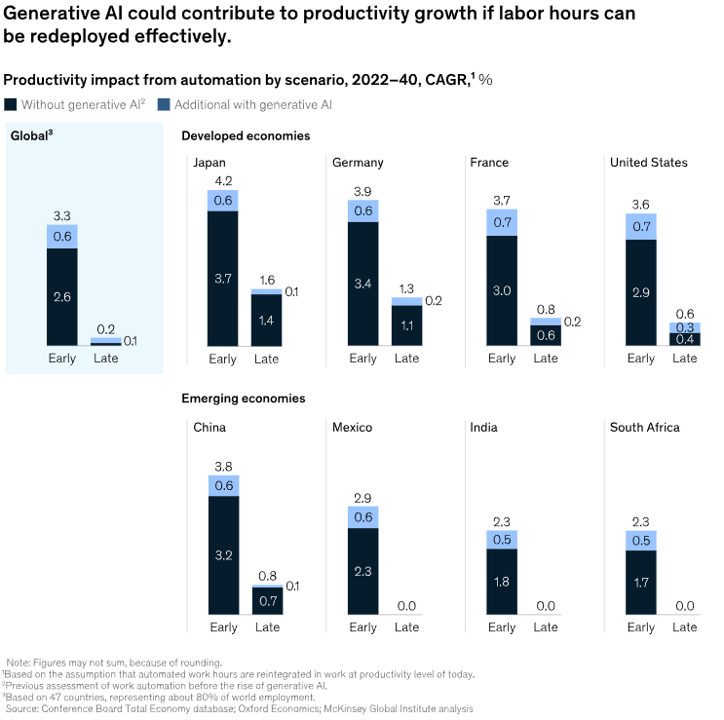

Key takeaways from the Q2-23 study by Mc Kinsey (see chart 4):

- “GAI has the potential to change the anatomy of work, augmenting the capabilities of individual workers by automating some of their individual activities”…

- “GAI’s could add the equivalent of $2.6 trillion to $4.4 trillion annually to global growth”

- “GAI could add 0.1 to 0.6 percent annually through 2040 to labor productivity growth”…

- “About 75 percent of the value that GAI creates falls across four areas: customer operations, marketing and sales, software engineering, and R&D”…

- “Banking, high tech, and life sciences are among the industries that could see the biggest impact, as a percentage of their revenues from generative AI.”

Chart 4: LT contribution of GAI to productivity

Different transmission mechanisms…

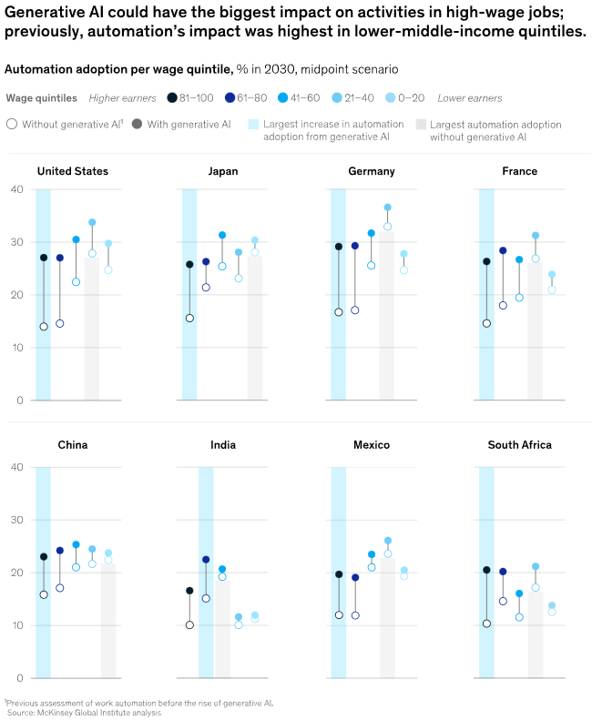

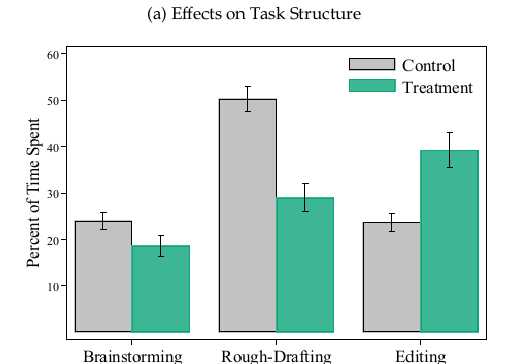

GAI is transformative and pervasive in nature. Large Language Models (LLM), like GPT popularized by Open AI and Microsoft, are democratizing AI for enterprises. Some dare to make the analogy with the arrival of the Web browsers – Netscape Navigator in the early 1990s – that triggered a chain of events changing the way we work, connect, consume, collaborate, and live. With GAI, what was once available to only a handful of large companies with access to massive supercomputing power, is likely to become available for all to customize and consume with a ‘copilot’ guiding us. This technology will integrate deeper into business and decision-making, hence primarily concern executives – withe collars – for the medium/long-term. See chart 5. Anecdotally, MIT studied the impact of ChatGPT on 444 white collar workers. They were asked to do writing and editing tasks along the lines of marketing, grant writing, data analysis, and human resources. The ChatGPT using group was 37% faster at completing tasks. In short, the system, greatly speeds up the “first draft” and “initial findings” but is more time consuming for final draft. See Chart 6.

Chart 5: Higher impact on high-wage jobs

Chart 6: ChatGPT impact

Another facilitator to a broad adoption of GAI comes from brighter – productive – Capex perspectives. Indeed, global policymakers have a renewed appetite for large public capex plans, linked to the climate disorder and security/defense (the new geopolitical world order). US, Europe, and China are committing to it for the long-term, with massive capital infusions. Productive capex should also benefit from the end of financial repression that, since the GFC, diverted corporates cash-flow into financial engineering. Private companies will no longer increase their debt (which has become onerous) to speculate or buy-back shares, but focus on gaining market share, improving competitiveness and so on.

…and new challenges

New York Times and other leading opinion journals are filled with articles about “dangers” of AI. It could for instance be perpetuating misinformation, empowering malicious actors, breaching privacy, infringing on intellectual property. Ultimately, it may become an easy scapegoat for populist leaders, as GAI will no doubt ultimately threaten jobs. GAI could substitute up to one fourth of current jobs (Goldman Sachs). Such a magnitude will make it quasi-impossible for displaced workers to adapt on time. Pressure on employment and wages is likely, which is a fundamentally disinflationnary.

Chart 7: GAI impact on sectors/industries

GAI is a pervasive tidal wave that will force organizations to revisit their business model and capex plans. YES, it is a game-changer for global economies through the channel of higher productivity, wage disinflation, but also greater macro-volatility and fragmentation

Headwinds to GAI adoption exist, like international relations, redeployment of worker time and policy-makers upcoming attempts to contain its side-effects. Its impacts will also greatly vary among country/region and sector/industry. The most educated/paid employees will be the first to be targeted / ¨uberized¨