Date: 11 June, 2020 - Blog

The ECB delivered a larger and longer than expected Pandemic Emergency Purchase Program (PEPP) envelope increase by €600bn to €1350bn until June 2021. This was slightly more than market forecasts. The ECB also announced that it will reinvest the PEPP holdings at least until 2022 year-end.

There was speculation about how the ECB would react to the German Constitutional Court’s ruling on QE. Lagarde showed the German Court that the ECB keeps its cold head. The ECB falls under the jurisdiction of the European Court of Justice, which had already judged that the QE follows its mandate. Lagarde hopes to find a good solution, which would not compromise the ECB or the primacy of European law.

The ECB disappointed corporate bond markets

As expectations had been running high for an extension of its purchase program to include “fallen angel” companies that held investment grade ratings before the coronavirus crisis hit. The ECB could still extend its coverage if needed. We do not expect the ECB to announce shortly further measures at the current juncture, even if during the press conference, President Lagarde was relatively balanced, albeit acknowledging the downside risks to the -8.7% growth forecast for 2020.

The biggest beneficiary of the ECB action appears to be once again Italy. This is understandable given that the decisions ensure that large-scale ECB purchases will continue at least into the middle of next year.

After all, large government issuance needs will continue for sure past the acute phase of the corona crisis. While the PEPP data released just a few days ago implies that the PEPP is not as flexible as the ECB has advertised, the larger and longer PEPP envelope will ensure the ECB will be able to continue supporting countries like Italy in significant magnitude for a longer time.

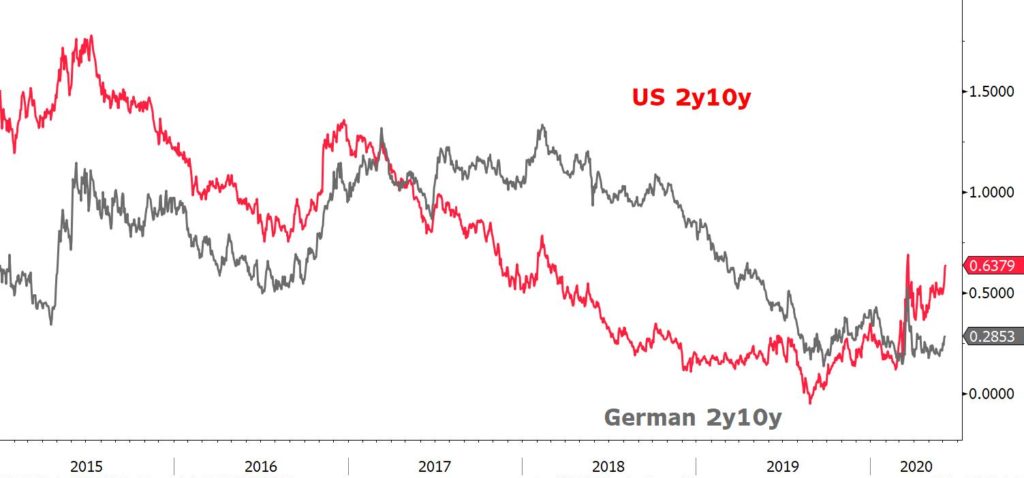

US and German slope of the yield curve (%)

Source: Bloomberg

German yields climbed a bit. The German curve will continue to steepen. First, the ECB will target its purchases to the shorter end of the curve, where most of the issuance takes place. Second, the recovery fund proposal will shift some credit risk for Germany to bear, and if the fund manages to lift hopes about an economic recovery even mildly, it should put some upward pressure on longer German bonds.

German and US long-end yields

Source: Bloomberg

- Peripheral spreads, mainly Italy, stay attractive, like credit spreads

- Long-end yields get out of their recent trends

- German yield curve steepening will continue